Blockchain technology has gained significant popularity, particularly after the success of Bitcoin. Many people believe that blockchain is merely a distributed ledger or database, but this is a misconception. Blockchain is much more than just a decentralized database; it is a unique data structure designed to solve critical issues in digital transactions, particularly in cryptocurrency.

To understand the importance of blockchain, let's explore its necessity through a short story.

The Initial Trust Issue in Cryptocurrencies

At an early stage, a user named X created a digital coin called Coin A. X announced that the total supply of Coin A would be 1000 coins and set an initial price of 1 Coin A = 1 USD. Through some marketing efforts, Coin A gained traction and its price started to rise due to its limited supply.

However, once the price reached a high value, X exploited the centralized nature of his database by adding another 1000 Coin A into his account without informing the users. This sudden increase in supply led to a collapse of trust, as investors realized they had been scammed. People lost faith in cryptocurrency, thinking that it was unreliable and could be manipulated by a central entity.

A New Approach: The Birth of Blockchain

After this event, a group of developers analyzed the situation and sought to find a way to make cryptocurrencies more trustworthy and decentralized. They identified the primary issues that needed to be addressed:

Problem 1: The Total Supply Must Remain Unchanged

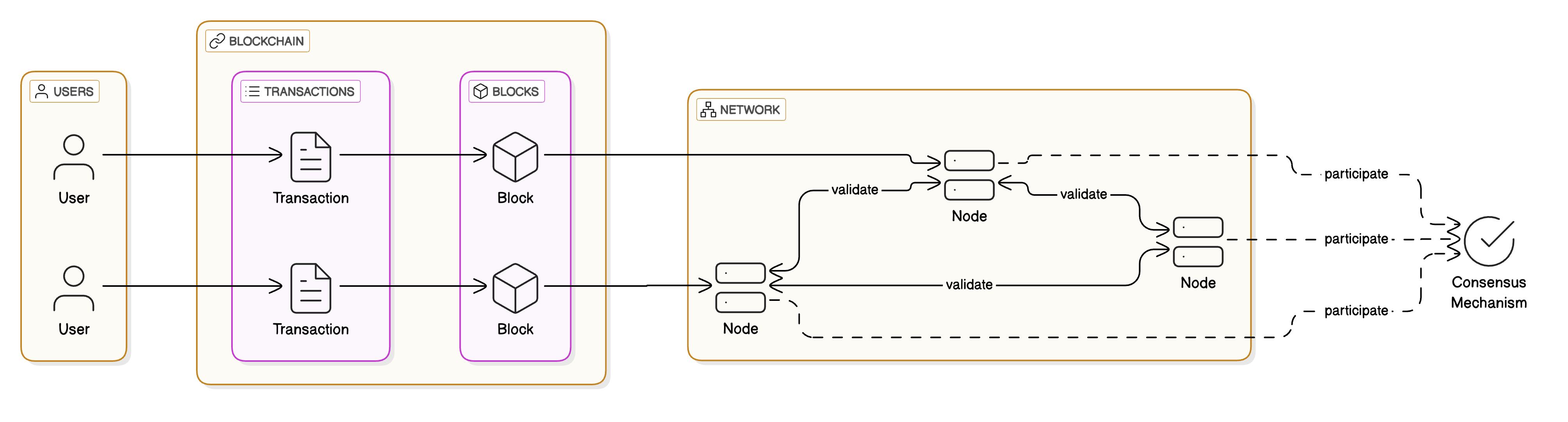

In the case of Coin A, the supply was manipulated by the creator, leading to inflation and loss of trust. To solve this issue, the developers designed a new data structure called Blockchain. In a blockchain, transactions and coin issuance are recorded in blocks, and once a block is added to the chain, it cannot be altered. This ensures that no one can change the total supply of a cryptocurrency once it has been set.

Each block in the blockchain contains:

- A list of transactions

- A timestamp

- A reference (hash) to the previous block

- A unique identifier (hash) of the current block

This structure guarantees that any attempt to modify a block would require altering all subsequent blocks, which is practically impossible due to the computational power required.

Problem 2: Preventing Unauthorized Changes to the Blockchain

Although blockchain itself ensures data integrity, there was still a risk that a single authority could control and rewrite the entire database. To solve this problem, the team implemented a Distributed Ledger System.

A distributed ledger means that the blockchain is not stored on a single server but is copied and maintained by thousands of computers (nodes) around the world. This decentralization ensures that:

- No single entity has control over the blockchain.

- Any modification attempt must be validated by the majority of the network.

- The system remains resistant to hacks and fraud.

Each node in the network keeps a copy of the entire blockchain and participates in a consensus mechanism (such as Proof of Work or Proof of Stake) to validate transactions. Once a new block is verified and added to the blockchain, it becomes immutable and cannot be altered by any single entity.

How Blockchain Restores Trust

With these two key solutions in place, blockchain became the backbone of modern cryptocurrencies, including Bitcoin and Ethereum. It ensures:

- Transparency: Every transaction is recorded on a public ledger that anyone can verify.

- Security: Cryptographic algorithms prevent tampering and unauthorized modifications.

- Decentralization: The absence of a central authority eliminates the risk of manipulation.

- Immutability: Once data is recorded, it cannot be changed or deleted.

Beyond Cryptocurrency: The Future of Blockchain

While blockchain was initially developed to solve issues in digital currencies, its applications extend far beyond finance. Today, industries such as healthcare, supply chain management, real estate, and voting systems are exploring blockchain technology for its security and transparency features.

For example:

- Supply Chain Management: Companies use blockchain to track the journey of goods from manufacturer to consumer, ensuring authenticity and reducing fraud.

- Healthcare: Medical records can be securely stored and accessed by authorized personnel without fear of unauthorized changes.

- Voting Systems: Blockchain can prevent election fraud by ensuring votes are tamper-proof and verifiable.

Conclusion

Blockchain technology has transformed the way we perceive digital transactions by introducing trust, security, and decentralization. By solving critical issues such as data manipulation and central control, blockchain has paved the way for a more transparent and secure digital economy. As industries continue to explore its potential, blockchain is poised to revolutionize various aspects of our lives beyond cryptocurrency.